As the old saying goes, buy when there is blood in the streets. There isn´t blood on the streets of Moscow at present but is certainly a bloodbath in Russian equities. Russia´s main stock index, the MOEX, has fallen 60% since October and 46% just since yesterday!

I´m not the Ukraine/Russia/NATO expert, and I doubt anyone is. But I do know that since Russia has had such a positive current account for decades, investments in Russia are held primarily by Russians. That matters because this selloff is not foreigners getting their money out of Russia, it´s just Russians fleeing equities. (Maybe it´s Russians getting their money out of the country before more sanctions hit. I don´t know about that, but it´s the same result.) Sooner or later Russians have no choice but to return to Russian equities. Sanctions, if they come as strongly as some think, mean that Russians have even fewer options than Russian equities for investment.

Here are three points to consider when thinking about whether Russian equities are a buy or a sell at present.

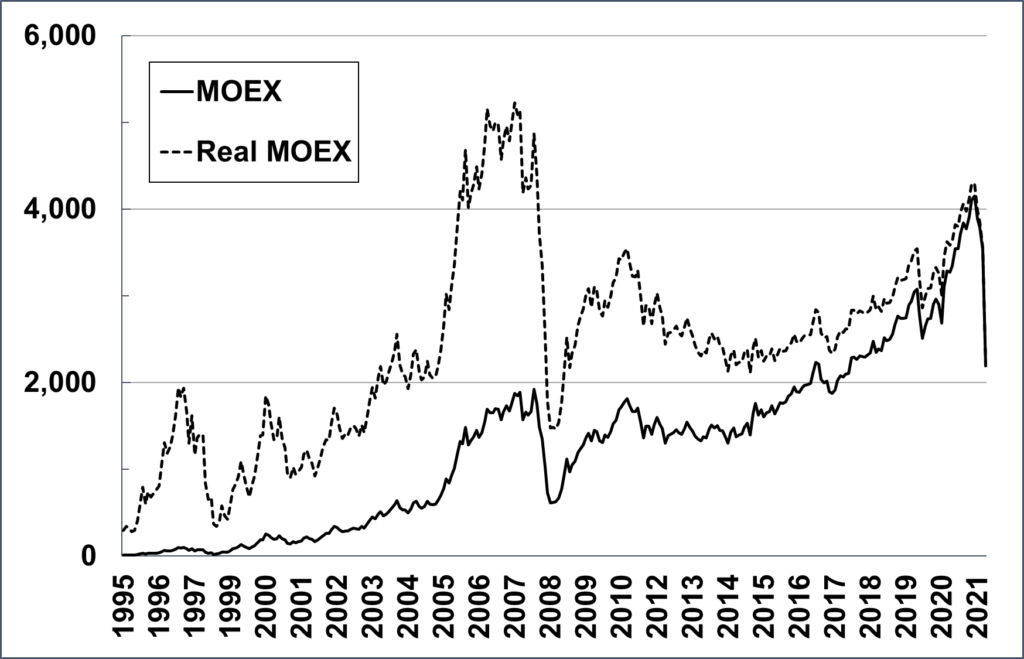

1. Adjusted for Russian inflation, the MOEX has wiped out all its gains since 2004 (see chart below). Real income in Russia is up nearly 50% over the same period. That´s a pretty large disconnect.

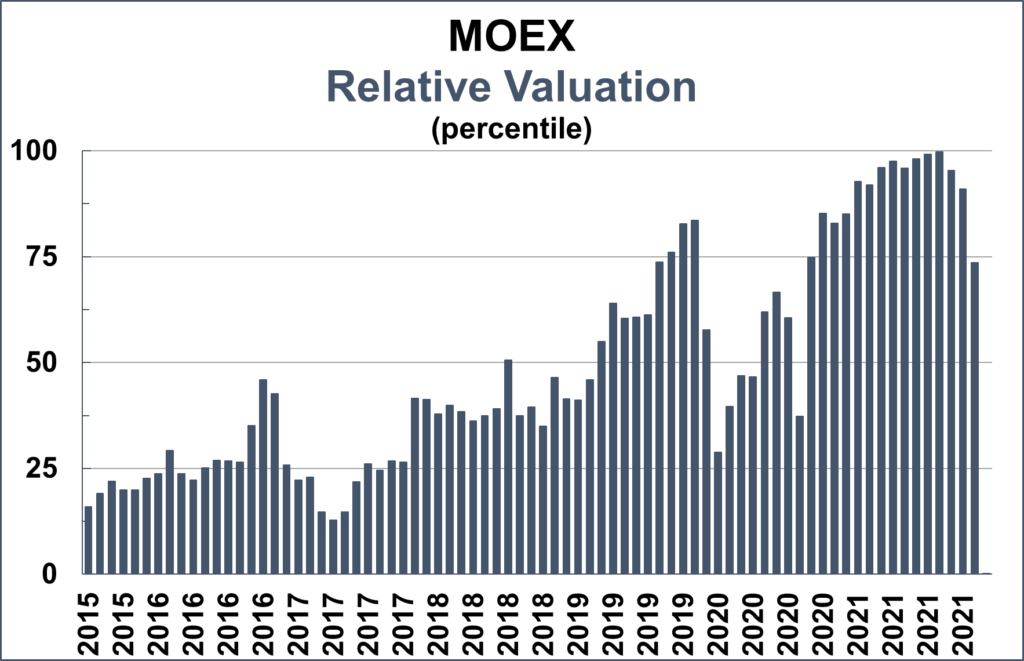

2. The best measure of whether equities are a buy or sell is to compare their prices to the other options available (buy a house, buy a stock, buy some food, etc. — real estate, financial investment, consume, etc.) I use a measure I developed called relative valuation that expresses a stock index´s price relative to a broad basket of goods. Check out the chart below.

I express the relative valuation of the MOEX as a percentile, so you can interpret it as the percent of the index´s history that it has been as highly valued as it currently is against a broad basket of goods (50th percentile implies it is fairly valued against the basket given its price history. 100th percentile means equities are more expensive than they ever have been, and 0th percentile means stocks are cheaper than ever). Back in September/October of last year, the MOEX was in the 99.5th percentile. It´s currently in the 0.2 percentile (that translates to a 3 sigma event). You can´t see the final bar on the relative valuation chart because it´s at zero. It implies Russian stocks are cheaper relative to Russian goods than ever in their history (admittedly, that goes back less than thirty years).

I don´t know about the exchange rate risk, but for Russians, equities have never been cheaper. Generally, great value within a country does not imply terrible value for foreigners.

3. In my books, I track the relative valuation for the main stock indexes for about forty countries. I´ve got price history going back to the 1950s for most of them, and of course, the Anglo world has stock price data going back several centuries. With all this data, I only have three cases of a major stock index being as undervalued as the MOEX is today. The FTSE in July 1940, the Dow Jones Industrial Average in June 1932, and the Transporation Average in December 1974.

There is no blood on the Russian streets yet. But Russian equities are currently valued at levels only seen in those rare cases where stellar investment returns result.